A Receipt Proves What You Paid. It Does Not Prove What You Can Withdraw.

You spent $2,400 on braces in 2022. You kept the receipt. Good.

Now it is 2026 and you want to reimburse yourself from your HSA. The IRS does not just want proof you paid $2,400. They want proof you have not already taken that $2,400 out tax-free.

That is two different questions. The receipt answers the first one. Only a reimbursement record answers the second.

What the IRS Actually Looks At

An HSA audit is not complicated. The IRS wants to match three things:

- ●A qualified medical expense happened (your receipt).

- ●You withdrew money from your HSA (your 1099-SA).

- ●The withdrawal was for an expense you had not already been reimbursed for.

Number 3 is the one that trips people up. Your HSA provider tracks contributions and withdrawals. They do not track which expense each withdrawal covers. That is your job.

If you cannot show which expenses your withdrawals covered, every distribution is potentially taxable. Plus a 20% penalty if you are under 65.

The $8,000 Scenario

Say you have $8,000 in unreimbursed medical expenses from the past five years. You pull $5,000 from your HSA in December.

The IRS sees $5,000 in distributions on your 1099-SA. They see you claimed $5,000 on Form 8889 Line 15 as qualified medical expenses. If they audit you, they want to know: which $5,000 out of the $8,000?

Without a record linking that $5,000 to specific expenses, you are stuck reconstructing it from memory. And you still have $3,000 in unreimbursed expenses left over. Pull that $3,000 next year and you have to prove it is new. Not the same $5,000 you already claimed.

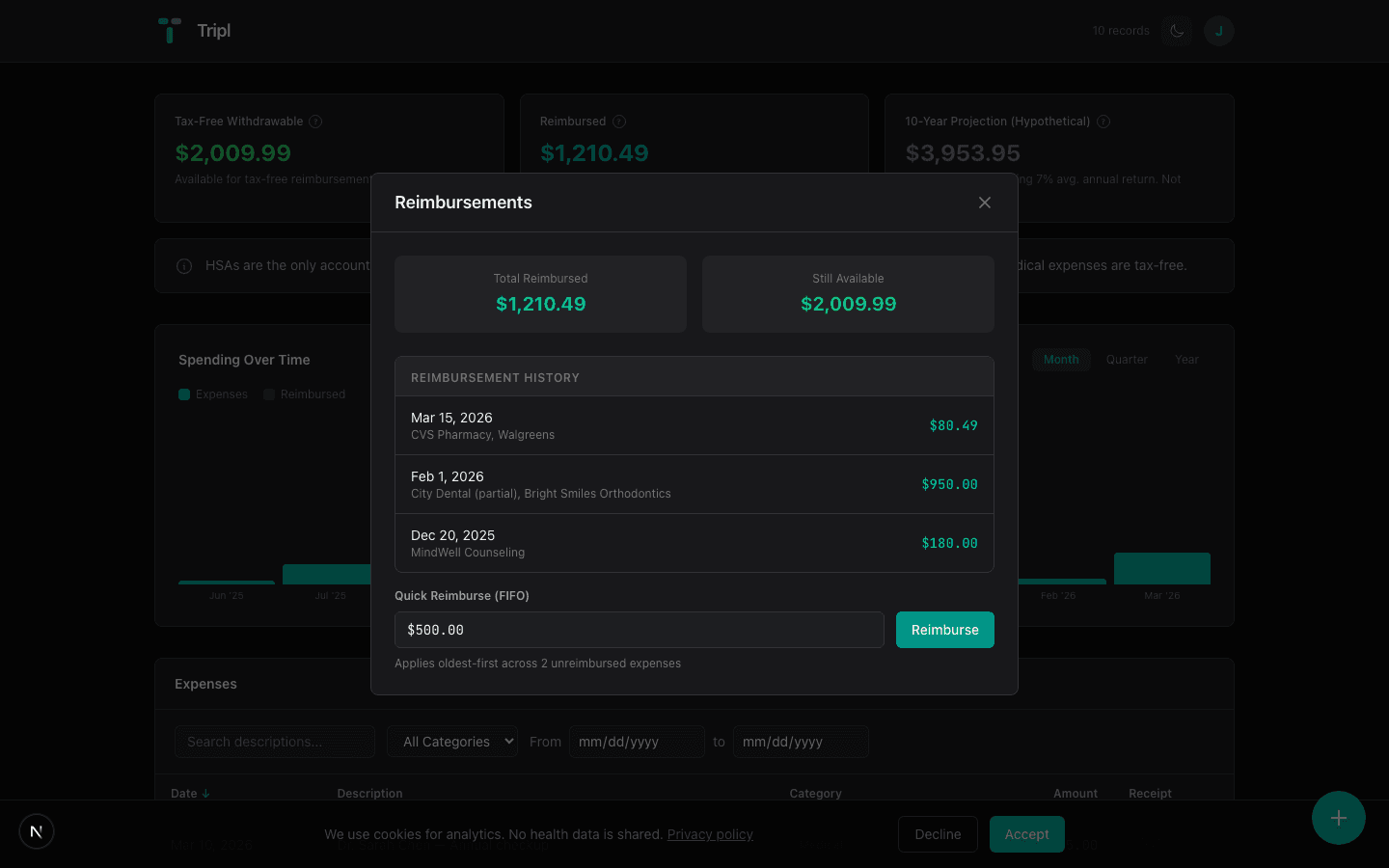

A reimbursement ledger solves this in 30 seconds. Date of reimbursement. Amount. Which expenses it covered. Done.

The Delayed Reimbursement Problem Gets Worse Over Time

The HSA reimbursement trick works because there is no time limit. You can pay out of pocket today and reimburse yourself 20 years later, tax-free.

That is a powerful strategy. It is also an organizational nightmare if you do not track what you have reimbursed.

After 10 years of paying out of pocket, you might have $30,000 to $50,000 in eligible expenses. Some are partially reimbursed. Some are fully reimbursed. Some you have not touched.

A shoebox of receipts tells you what you spent. It does not tell you what is still available. The number the IRS cares about is the available balance: total eligible expenses minus total reimbursements taken.

Real Numbers: The Audit Scenario

Here is a concrete example.

| Year | Expense | Amount | Reimbursed? | Amount Reimbursed |

|---|---|---|---|---|

| 2020 | ER visit | $3,200 | Partial | $1,500 |

| 2021 | Physical therapy | $2,800 | No | $0 |

| 2022 | Braces | $2,400 | Yes | $2,400 |

| 2023 | Prescriptions | $1,100 | No | $0 |

| 2024 | Lab work | $950 | No | $0 |

2020

- Expense

- ER visit

- Amount

- $3,200

- Reimbursed?

- Partial

- Amount Reimbursed

- $1,500

2021

- Expense

- Physical therapy

- Amount

- $2,800

- Reimbursed?

- No

- Amount Reimbursed

- $0

2022

- Expense

- Braces

- Amount

- $2,400

- Reimbursed?

- Yes

- Amount Reimbursed

- $2,400

2023

- Expense

- Prescriptions

- Amount

- $1,100

- Reimbursed?

- No

- Amount Reimbursed

- $0

2024

- Expense

- Lab work

- Amount

- $950

- Reimbursed?

- No

- Amount Reimbursed

- $0

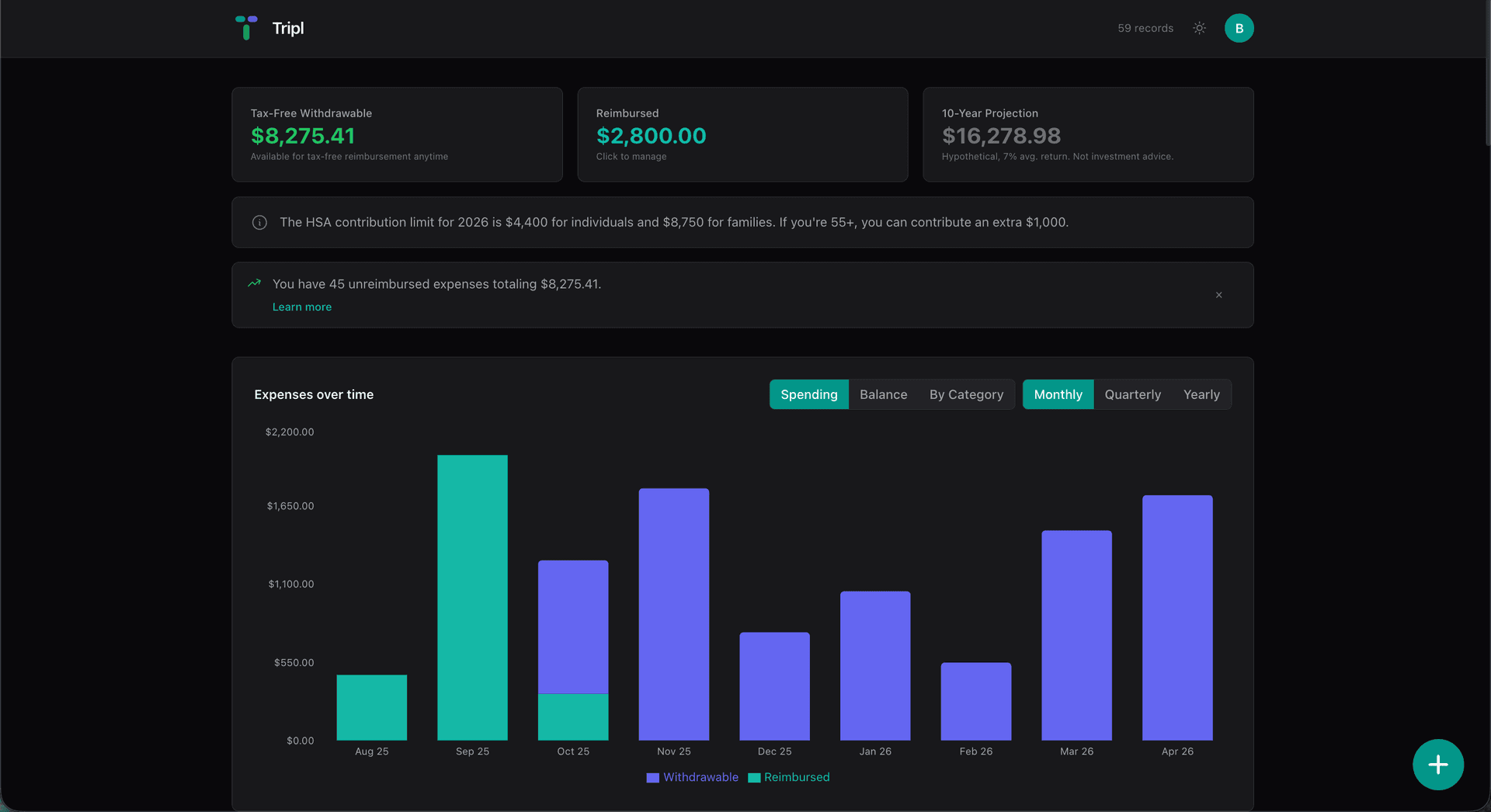

Total expenses: $10,450. Total reimbursed: $3,900. Available tax-free: $6,550.

Without this table, you are guessing. With it, you can hand the IRS a one-page summary that matches your 8889 line by line.

The partially reimbursed ER visit is the tricky one. You took $1,500 of a $3,200 expense. That means $1,700 is still available. A receipt alone does not show the $1,500 you already withdrew. Only the reimbursement record does.

Your HSA Provider Does Not Track This For You

This is the part that surprises people. Fidelity, HSA Bank, Lively, HealthEquity. None of them track which expense each withdrawal covers.

They report total distributions to the IRS. You report whether those distributions were qualified. The matching is on you.

Some people use spreadsheets. Some use folders of receipts with sticky notes. Some just hope they never get audited.

Hope is not a record-keeping strategy.

What a Good Reimbursement Record Looks Like

It does not need to be complicated. It needs four columns:

- ●Date of expense and what it was

- ●Amount of the expense

- ●Date of reimbursement (when you pulled from your HSA)

- ●Amount reimbursed (partial or full)

That is it. If you can produce this for every dollar you have withdrawn from your HSA, you are audit-ready.

The receipt proves the expense happened. The reimbursement record proves you have not double-dipped. You need both.

The Tax-Free Number That Matters

Most HSA tools focus on your account balance. That is important, but it is only half the picture.

The other number is your available tax-free total. Every qualified expense you have paid. Minus every dollar you have already reimbursed. This is the maximum you can withdraw without owing tax or penalties.

If you do not know that number, you do not know what your HSA is actually worth to you.

Tripl Tracks This Automatically

Tripl logs every expense and every reimbursement in a single ledger. When you reimburse, it records the date, amount, and exactly which expenses the reimbursement covers.

Your available tax-free total updates in real time. No spreadsheets. No sticky notes. One number, always current.

When tax season comes, export a PDF report with every reimbursement matched to its expenses. If the IRS asks, you hand them the report.

Try Tripl free at triplapp.com

Stop Thinking About Receipts. Start Thinking About Ledgers.

A receipt is a snapshot. A ledger is the asset. The IRS audits the ledger, not the shoebox. Build the ledger now and the next 30 years of tax-free withdrawals defend themselves.

Frequently Asked Questions

Does the IRS actually audit HSA distributions?

Yes. HSA audits are part of standard income tax audits. The IRS receives your 1099-SA from your provider and your Form 8889 with your return. If the numbers do not match or look unusual, they can request documentation.

How long should I keep HSA records?

The IRS can audit returns up to 3 years back (6 years if they suspect underreporting). If you are using the delayed reimbursement strategy, keep records longer. As long as the expenses remain unreimbursed. That could be decades.

Can I fix my records if I have not been tracking?

Yes. Go through your HSA provider's distribution history and match each withdrawal to an expense. It is tedious but doable. Going forward, track every reimbursement as it happens.

What if I accidentally reimburse more than I am eligible for?

The excess amount is taxable income plus a 20% penalty if you are under 65. After 65, it is taxable income only. This is exactly the kind of mistake a reimbursement ledger prevents.

This is educational content, not financial or tax advice. Consult a qualified professional before making decisions about your HSA.